Plenty of news today from big pharma with speculation surrounding a Pfizer/AstraZeneca tie up and a major announcement from GSK/Novartis on an asset swap. Both are an illustration that the sector is trying to find its way in an increasingly hostile regulatory environment, where drug development costs are now running in several billions per successful candidate.

Shares in AstraZeneca (AZN) are 7.9 percent higher today to £40.79 after the Sunday Times reported that Pfizer had approached it to propose a £60 billion ($101 billion) takeover. Talks are no longer continuing but the market is hoping that Pfizer will come back for a second bite of the cherry. At the current share price, AZ has a market cap of £51 billion.

In addition, Novartis and GlaxoSmithKline (GSK) have agreed to swap a series of assets in a multi-billion dollar deal that will see the pair pool their consumer products units in a new joint-venture. GSK’s share are up over 5% on the news to £16.43 with the prospect of a £4 billion return to shareholders and revenues increasing by £1.3 billion to £29.6 billion.

GSK will sell its portfolio of cancer drugs to Novartis for at least $14.5 billion, with a potential further $1.5 billion in milestone payments subject to the success of a trial into a new combination therapy involving existing GSK cancer drugs. The deal will also see GSK buy the Novartis vaccines business for $5.25 billion, with GSK receiving $7.8 billion net from the transactions. They will also combine their consumer healthcare businesses , which will now be controlled by GSK with its 63.5% share of the joint venture. Novartis also separately announced it will sell its animal health business to Eli Lilly for $5.4 billion.

I am pretty skeptical that Pfizer would want to swallow AstraZeneca for the sort of sums being speculated about given the less than successful acquisition of Wyeth for $68 billion in 2009 and Pharmacia deal in 2002 as well as a forthcoming patent expiry cliff for Astra which makes it a less than enticing prospect. With the shares of AZN at these sort of levels over £40 a share, I certainly would be taking profits if I was holding, as the Sunday Times article indicates that talks have stalled (the shares were trading around £30 in the summer of 2013).

Pfizer has had its fingers burnt before with expensive mega deals. Its acquisition of Pharmacia UpJohn (formed from the merger of U.S. Upjohn and Swedish Pharmacia in 1995) for $60 billion in an all share deal went badly wrong when two of its key blockbuster arthritis drugs called COX2 inhibitors were found to be associated with potentially serious side effects relating to increased risk of heart attack and stroke. After an FDA review in 2005, Celebrex (celecoxib) had its labeling amended and second generation COX2 Bextra (valdecoxib) was withdrawn from sale.

After years of underperformance at Astra, Pascal Soriot joined the company as Chief Executive Officer on 1 October 2012, taking over from the hapless David Brennan. Soriot joined AstraZeneca from Roche AG where he served as Chief Operating Officer of the company’s pharmaceuticals division and was Chief Executive Officer of Genentech.

Fourth-quarter 2013 earnings at Astra excluding restructuring costs declined 26% at constant exchange rates to $1.98 billion (£1.21 billion), with forecasts of a revenue decline in a low-to-mid single digit percentage at constant exchange rates and earnings per share excluding some items will decrease by a percentage somewhere in the teens. The company is being hit by the forthcoming patent expiry of heartburn treatment Nexium, asthma product Symbicort in 2014 and cholesterol reducer Crestor in 2016 which represent over a third of the companies revenues at $3.87 billion, $3.0 billion and $5.62 billion respectively.

The company says it has 11 medicines in late stage trials, with 19 potentially entering late stage trials in the next two years but unfortunately AstaZeneca hasn’t had too much luck in clinical trials over recent years with many promising new drugs failing to hit milestones. In December 2013 the company bought Bristol-Myers Squibb’s stake in their diabetes JV for $4.2 billion.

Pharmaceutical company shares have had a great run over the last few years. The L&G Global Health and Pharmaceutical Index fund has made 58% in the last 3 years (up 8% in the last year) after a period of significant underperformance. Larger companies have under performed the biotech sector with the SPDR S&P biotech ETF gaining 25% in the last year alone despite the recent sell off in biotechs and technology companies.

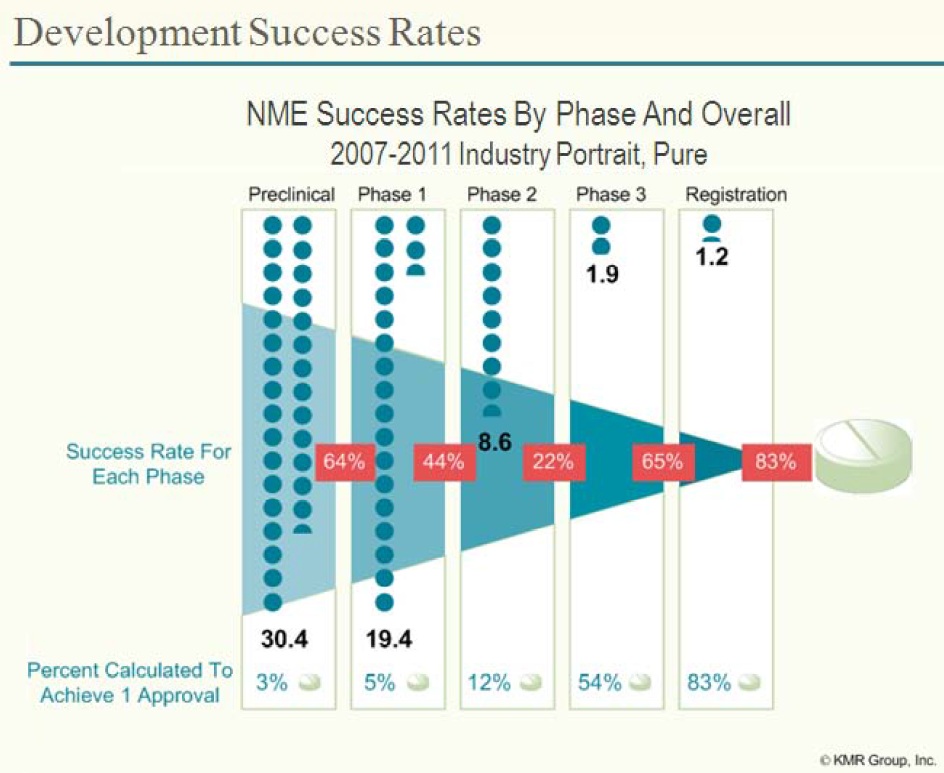

Big pharma has been heavily acquisitive of smaller companies of late highlighting the fact that as few as 16% of new drugs ever make it through clinical trials with the average cost for larger companies around $5 billion per drug taking into account the many failures. A 2012 article in Nature Reviews Drug Discovery says the number of drugs invented per billion dollars of R&D invested has been cut in half every nine years for half a century.

As well as the huge costs and high failure rates of getting new drug compounds to market, regulators around the world have increased scrutiny of new drug applications which means that many are taking much longer to be approved.

Though drug expenditure in the developed world continues to rise, health authorities are increasingly scrutinising drug costs and putting pressure on pharmaceutical companies to reduce pricing and on doctors to prescribe generic rather than branded products. Generics, whose ingredient has gone off patent, are often 90% cheaper than their branded equivalents.

After the big merger deals a few years ago failed to boost R&D productivity, companies like GSK and Novartis are now focusing their resources on core competencies and trying to streamline their development portfolios and lessen the impact of major patent expiries. The news of the last few days, may mean a new era of asset swaps and collaboration rather than the big takeover deals of the past. We will see.

Contrarian Investor UK

IMPORTANT: The posts I make are in no way meant as investment suggestions or recommendations to any visitors to the site. They are simply my views, personal reflections and analysis on the markets. Anyone who wishes to spread bet or buy stocks should rely on their own due diligence and common sense before placing any spread trade.

by contrarianuk

Big pharma in focus this morning as AstraZeneca and GSK grab the headlines

Apr 22, 2014 at 9:50 am in Market Commentary by contrarianuk

Plenty of news today from big pharma with speculation surrounding a Pfizer/AstraZeneca tie up and a major announcement from GSK/Novartis on an asset swap. Both are an illustration that the sector is trying to find its way in an increasingly hostile regulatory environment, where drug development costs are now running in several billions per successful candidate.

Shares in AstraZeneca (AZN) are 7.9 percent higher today to £40.79 after the Sunday Times reported that Pfizer had approached it to propose a £60 billion ($101 billion) takeover. Talks are no longer continuing but the market is hoping that Pfizer will come back for a second bite of the cherry. At the current share price, AZ has a market cap of £51 billion.

In addition, Novartis and GlaxoSmithKline (GSK) have agreed to swap a series of assets in a multi-billion dollar deal that will see the pair pool their consumer products units in a new joint-venture. GSK’s share are up over 5% on the news to £16.43 with the prospect of a £4 billion return to shareholders and revenues increasing by £1.3 billion to £29.6 billion.

GSK will sell its portfolio of cancer drugs to Novartis for at least $14.5 billion, with a potential further $1.5 billion in milestone payments subject to the success of a trial into a new combination therapy involving existing GSK cancer drugs. The deal will also see GSK buy the Novartis vaccines business for $5.25 billion, with GSK receiving $7.8 billion net from the transactions. They will also combine their consumer healthcare businesses , which will now be controlled by GSK with its 63.5% share of the joint venture. Novartis also separately announced it will sell its animal health business to Eli Lilly for $5.4 billion.

I am pretty skeptical that Pfizer would want to swallow AstraZeneca for the sort of sums being speculated about given the less than successful acquisition of Wyeth for $68 billion in 2009 and Pharmacia deal in 2002 as well as a forthcoming patent expiry cliff for Astra which makes it a less than enticing prospect. With the shares of AZN at these sort of levels over £40 a share, I certainly would be taking profits if I was holding, as the Sunday Times article indicates that talks have stalled (the shares were trading around £30 in the summer of 2013).

Pfizer has had its fingers burnt before with expensive mega deals. Its acquisition of Pharmacia UpJohn (formed from the merger of U.S. Upjohn and Swedish Pharmacia in 1995) for $60 billion in an all share deal went badly wrong when two of its key blockbuster arthritis drugs called COX2 inhibitors were found to be associated with potentially serious side effects relating to increased risk of heart attack and stroke. After an FDA review in 2005, Celebrex (celecoxib) had its labeling amended and second generation COX2 Bextra (valdecoxib) was withdrawn from sale.

After years of underperformance at Astra, Pascal Soriot joined the company as Chief Executive Officer on 1 October 2012, taking over from the hapless David Brennan. Soriot joined AstraZeneca from Roche AG where he served as Chief Operating Officer of the company’s pharmaceuticals division and was Chief Executive Officer of Genentech.

Fourth-quarter 2013 earnings at Astra excluding restructuring costs declined 26% at constant exchange rates to $1.98 billion (£1.21 billion), with forecasts of a revenue decline in a low-to-mid single digit percentage at constant exchange rates and earnings per share excluding some items will decrease by a percentage somewhere in the teens. The company is being hit by the forthcoming patent expiry of heartburn treatment Nexium, asthma product Symbicort in 2014 and cholesterol reducer Crestor in 2016 which represent over a third of the companies revenues at $3.87 billion, $3.0 billion and $5.62 billion respectively.

The company says it has 11 medicines in late stage trials, with 19 potentially entering late stage trials in the next two years but unfortunately AstaZeneca hasn’t had too much luck in clinical trials over recent years with many promising new drugs failing to hit milestones. In December 2013 the company bought Bristol-Myers Squibb’s stake in their diabetes JV for $4.2 billion.

Pharmaceutical company shares have had a great run over the last few years. The L&G Global Health and Pharmaceutical Index fund has made 58% in the last 3 years (up 8% in the last year) after a period of significant underperformance. Larger companies have under performed the biotech sector with the SPDR S&P biotech ETF gaining 25% in the last year alone despite the recent sell off in biotechs and technology companies.

Big pharma has been heavily acquisitive of smaller companies of late highlighting the fact that as few as 16% of new drugs ever make it through clinical trials with the average cost for larger companies around $5 billion per drug taking into account the many failures. A 2012 article in Nature Reviews Drug Discovery says the number of drugs invented per billion dollars of R&D invested has been cut in half every nine years for half a century.

As well as the huge costs and high failure rates of getting new drug compounds to market, regulators around the world have increased scrutiny of new drug applications which means that many are taking much longer to be approved.

Though drug expenditure in the developed world continues to rise, health authorities are increasingly scrutinising drug costs and putting pressure on pharmaceutical companies to reduce pricing and on doctors to prescribe generic rather than branded products. Generics, whose ingredient has gone off patent, are often 90% cheaper than their branded equivalents.

After the big merger deals a few years ago failed to boost R&D productivity, companies like GSK and Novartis are now focusing their resources on core competencies and trying to streamline their development portfolios and lessen the impact of major patent expiries. The news of the last few days, may mean a new era of asset swaps and collaboration rather than the big takeover deals of the past. We will see.

Contrarian Investor UK

IMPORTANT: The posts I make are in no way meant as investment suggestions or recommendations to any visitors to the site. They are simply my views, personal reflections and analysis on the markets. Anyone who wishes to spread bet or buy stocks should rely on their own due diligence and common sense before placing any spread trade.