There is a question worth asking before you invest in any business where the primary asset walks out of the door at six o’clock every evening: when things go well, who actually benefits? And when things go badly, who pays?

The answer, in most so-called “people businesses,” follows a pattern that is consistent enough to be called a structural feature rather than a coincidence. Those running the business — the partners, the rainmakers, the senior fee earners — tend to capture the upside. The shareholders tend to absorb the downside. And in the middle, when times are merely ordinary, outside investors often find themselves in the uncomfortable position of having taken all the equity risk for a return that barely justifies it.

This is not a story about bad actors or wilful misconduct. It is a story about how incentive structures, left unchallenged, tend to compound in favour of those who designed them.

The Good Years

In a good year, a people business is a compelling thing. Fee income grows, case wins come in, deals get done, and the P&L looks healthy. But before that profit reaches the shareholders, it passes through several layers of extraction. Salaries at the top end of the market. Bonuses calibrated to performance. Carried interest, performance fees, or profit-share arrangements that, by design, take a significant slice of the upside before it is ever allocated to equity holders.

This is often defensible in isolation. The argument runs that without retaining the talent that generates the returns, there would be no returns to distribute at all. And there is truth in that. A litigation finance business without experienced case handlers, or an asset manager without fund managers with credible track records, is worth very little. The people are genuinely the product.

But the effect on shareholders is real regardless of the justification. By the time bonuses are paid, performance fees crystallised, and carry distributed, what remains for the public market investor can look thin — particularly relative to the risk they took on by providing the capital in the first place. They get paid last. And the architecture of the fee structure, often embedded deep in employment contracts and partnership agreements that predate any investor relations conversation, ensures that this ordering is more or less immovable.

The Bad Years

Then comes the difficult period. Markets turn, deal flow dries up, a key case goes the wrong way, or the macro environment that underpinned the whole model shifts. Revenue falls. Costs, particularly people costs, prove stickier than expected. The business starts burning cash.

At this point, something interesting happens. The same shareholders who spent the good years watching performance fees erode their returns are now asked to participate in a capital raise. A placing is announced — typically at a discount, typically dilutive, and typically framed as an opportunity to support the business through a temporary period of difficulty. Enough investors subscribe, the raise completes, and the company lives to fight another day.

What is rarely said plainly is that this represents a transfer of risk that was baked into the model from the beginning. The people who extracted value during the good years are not writing cheques during the bad ones. It is the shareholders — both existing holders who are diluted and new participants who are invited in at the bottom — who bear that burden. The profits, in other words, were privatised. The losses are socialised.

The Ownership Illusion

One might reasonably assume that examining the shareholding structure would give some clarity on whether a business is genuinely aligned with outside investors. In practice, it often doesn’t.

In small-cap companies particularly, it is common to find founders or senior management holding significant equity stakes. On the surface, this looks reassuring — skin in the game, interests aligned, all the phrases that appear in investor presentations. But large insider holdings do not automatically mean what they appear to mean.

Sometimes a controlling stake exists primarily to maintain control: to keep the board composed of loyalists, to prevent activist pressure from gaining traction, and to ensure that compensation structures remain calibrated in the interests of management rather than shareholders at large. The stake is a governance lever, not a statement of confidence in the equity. The insider is not holding because they think the shares are cheap. They are holding because selling would mean ceding influence over a business that, structured as it is, continues to generate attractive personal returns regardless of what the share price does.

The absence of dividends tends to confirm the picture. A business that has been consistently profitable for several years and consistently finds reasons not to return cash to shareholders — capital requirements, reinvestment opportunities, conservative balance sheet management — is a business where the question of who the capital is being preserved for deserves a careful answer. In too many cases, that answer is not the outside shareholder.

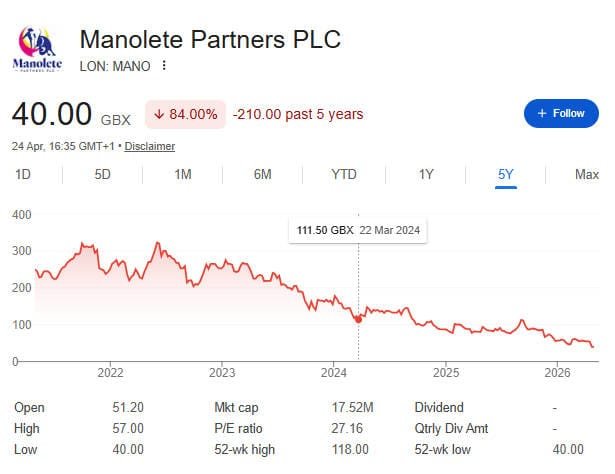

Case in Point: Manolete Partners

As with all ‘people businesses’ the question arises as to who benefits during the good times and who pays during the bad times.

When things are going well, bonuses and performance fees wipe out shareholder returns. They get paid first….we get the scraps.

In the bad times when the company needs to raise funds then it is shareholders on the line for that.

Keep the profits and socialise the losses.

Or at best….get thrown a few scraps in the good times but be on the hook for the losses during the bad times.

Admittedly, it’s a lumpy model. A few huge wins can mean the timing works out for shareholders – a win is so large it would be embarrassing to not share that out.

But on the whole, as you say, I think the model is broken.

You can look at the shareholding structure to see whether it is skewed to benefit shareholders, but sometimes even that is unhelpful. With tiny market cap companies sometimes large insiders keep their stake just to have control of the business and to keep the bonuses and performance at levels that suit them, rather than shareholders more generally.

The Succession Problem

The most reliable catalyst for change in these businesses is usually a large shareholder who has grown tired of the arrangement and wants a proper exit at a fair price. Activist pressure, a strategic review, a takeover approach — these are the moments when the interests of inside and outside shareholders are most likely to be temporarily aligned around a single number.

But people businesses have a way of neutralising even this. There is almost always an heir to the throne. A trusted deputy, a long-serving partner, a successor who has been quietly prepared for the transition and who — crucially — shares the incumbent’s views on how the business should be run and how it should be compensated. The change of leadership is real. The change of culture is not. The baton passes smoothly, the compensation structures survive intact, and the cycle continues for another cycle.

This is why the typical value catalyst in these businesses is so elusive. Unlike an industrial company sitting on underutilised assets, or a retailer whose property portfolio is worth more than its market cap, the path to value realisation in a people business runs directly through the people — and they are rarely motivated to unlock it.

The Exceptions

None of this is to say that all people businesses are traps. Some of them are excellent investments, and the characteristics that separate the good from the bad are usually visible to anyone who looks carefully enough.

The businesses that genuinely work for shareholders tend to share a few features. Their models have compounding properties that go beyond individual fee earners — proprietary systems, data advantages, brand equity, or scale benefits that make the business structurally valuable independent of any single person. Their compensation structures include meaningful clawback provisions that tie individual payouts to long-term outcomes rather than annual results. Their insiders own equity at market prices rather than through options struck at favourable levels. And they return cash — consistently, predictably, in a way that signals genuine confidence that the business generates more than it needs.

Dividends are underrated as a signal in this context. A business that pays a growing dividend is a business that has run out of convincing reasons to retain the cash. That is, in its own quiet way, a statement of shareholder primacy. Its absence is, equally, a statement of something else.

What to Look For

The question every investor should ask before buying into a people business is a simple one: if the three most important people left tomorrow, what would I own?

If the honest answer is a brand, some contracts, and a leasehold office, then the equity is more fragile than the valuation implies. If the answer includes proprietary technology, sticky client relationships that genuinely sit with the institution rather than the individual, or a model that has demonstrated it can survive personnel transitions, then the picture is different.

Beyond that, the checklist is short but revealing. Is the fee structure genuinely aligned with shareholder outcomes, or does it prioritise short-term extraction? Do insiders hold equity because they believe in the business, or because control suits them? Is cash being returned, or perpetually retained? And when you read the remuneration report — which most investors skip — does the structure feel like something designed to attract and retain talent, or something designed to extract maximum value from a captive shareholder base?

The people business model is not broken by definition. But it has a gravity of its own, and that gravity pulls in a predictable direction. The investors who do well in this space tend to be the ones who identified, early, that the business had found a way to fight that gravity — not the ones who assumed it wasn’t there.

The pattern described here is not unique to any single company or sector. It recurs across litigation finance, asset management, recruitment, professional services, investment banking, and anywhere else where the balance sheet is secondary to the talent. Identifying it is not cynicism. It is the beginning of good due diligence.

Litigation Finance & Legal Services Manolete’s own backyard. Case outcomes are binary and lumpy, fee structures are opaque, and the people originating and managing cases can extract performance fees regardless of whether shareholders have made back their cost of capital. Burford Capital is the large-cap version of this conversation.

Asset Management & Fund Managers Perhaps the most textbook example. Management fees cover salaries in the bad years; performance fees supercharge pay in the good ones. When AUM falls and the fund struggles, it’s shareholders in the listed vehicle who bear the pain of redemptions, staff departures, and declining earnings — while the partners who already crystallised their carry are largely insulated. Think boutique listed fund managers: Gresham House, Polar Capital, River and Mercantile before its acquisition.

Private Equity & Venture Capital (Listed Vehicles) Carried interest structures mean the general partners take 20% of profits above a hurdle. When the cycle turns and portfolio valuations collapse, those carry payments don’t reverse. Shareholders in listed PE vehicles like Apax Global Alpha or HarbourVest watch NAV erode while management fees continue ticking.

Investment Banking Boutiques The bonus pool at a good boutique in a strong M&A year can dwarf shareholder returns. In lean years, the talent simply walks. The human capital — which is the entire business — is not owned by shareholders. They own the brand, the balance sheet, and the downside.

Recruitment & Staffing Firms Less egregious but structurally similar. In good markets, billers and directors earn outsized commission and bonuses. When the cycle turns and hiring freezes hit, the fixed cost base crushes margins quickly and shareholders absorb the earnings collapse while the best fee earners often defect to competitors.

Professional Services (Accountancy, Consulting, PR rollups) Listed rollups of accountancy or consulting firms are a particularly interesting case. The selling partners often roll equity but also retain earn-out structures that prioritise their payout. Organic staff are incentivised with schemes that dilute outside shareholders. The people who matter most to the business are economically protected in ways the public market investor simply is not.

Sports & Entertainment Agencies Talent representation businesses — whether sports agents or music management rollups — are almost entirely dependent on key relationships. Those relationships sit with individuals, not with the company. When the star agent leaves, they take the clients. Shareholders are left with an office lease and a brand.

Real Estate & Property Advisories Listed property consultancies share many of the same traits. Transaction-based bonuses in hot markets, cost-cutting and impairments in cold ones. The deal-makers are well compensated throughout; shareholders ride the cycle.

The tell-tale signs cut across all of these:

- Revenue is relationship-dependent and walks out the door

- Compensation is front-loaded and not clawed back

- Capital raises tend to come at the worst possible time

- Dividends are inconsistent or absent

- Insider stakes are large enough for control but not large enough to genuinely align incentives

- The succession plan conveniently preserves the existing compensation culture

The businesses that escape this trap tend to be the ones where the model has genuine intellectual property, proprietary systems, or scale advantages that mean the business is worth more than the sum of its people — and where management have enough skin in the game at market prices (not options) to feel the same pain as outside investors.

Those businesses exist. They’re just rarer than the prospectus would have you believe.