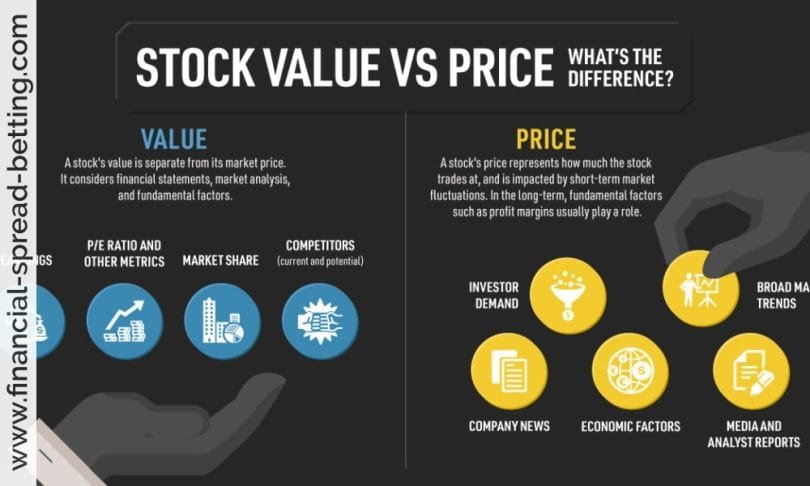

Knowing how to value a stock or an asset is absolutely vital in deciding when to buy and sell, to make a profit and avoid a loss. Investors research and buy shares into companies they believe will continue growing while selling those they think will stop growing.

It is important to appreciate that financial markets are forward-looking and trade on perception and assumptions about the future of an enterprise. Investors will often seek to anticipate events and then price their market view of it and what it means for an enterprise’s valuation. Having said that, there are several key valuation techniques, some of which are outlined below.

Technical Analysis or Fundamental Trading?

Cashflow

Cash is a company’s life-blood. Irrespective of how company is performing, if it runs out of money, it will default. A company has to be able to pay its employees, business suppliers and shareholders. Shareholders will usually expect a dividend unless the company retains cash to grow itself and increase share value. Some would think that a company’s bottom line, its net income, is represented by the cash the enterprise has generated. But this is not the case. Net income is what is left over after expenses are subtracted from revenues.

As a trader you should be more interested in cash creation than earnings after adjustments so you should check the company’s free-cash-flow, which represents its ‘true’ cash flow and what is has available to invest in new projects or to pay investor dividends. A market drop in cash generation when earnings are supposedly increasing could be an early sign that a company is in trouble. A company’s free-cash-flow is its net income adding both depreciation and amortization expenses, but then minus the company’s changes in working capital and capital expenditures. See below.

Net income

+ Amortization + Depreciation ? Changes in working capital ? Capital expenditures = Free cash flow

Traders sometimes also use company’s free-cash-flow data in a discounted-cash-flow analysis to check whether its stock price is expensive in relation to the cash the company is able to generate. Theoretically a discounted-cash-flow analysis is one of the best ways to value an enterprise and the idea behind it is to work out how much a company’s future cashflow is worth in today’s money (this is referred to as the company’s intrinsic value).

Beware that creative accounting can increase a companies profits at the expense of cashflow. Cashflow is what goes in and out of the bank account and therefore is very difficult to manipulate so a lot of investors give it priority over the profit and loss section of the accounts. A company can buy or manufacture a lot of stock and by creative accounting may invoice it as sold before its been paid for or even left the shop. Cashflow will expose this. That’s how Worldcom and Enron accounts first set alarm bells ringing. That why a lot of fund managers will only buy on a price: cashflow basis. So in this respect pay attention to three particular items: sales, earnings before interest and tax (EBIT, or operating profit) and cash from operations. If profits and sales are going up and cash is falling, something may be terribly wrong.

You can also use cashflow analysis to discover potential before they start crashing. The following link is worth bookmarking imo as it shows how a CFO can try to hide problems by manipulating earnings at the expense of cash items such as inventories. You will need to expand the size of the cashflow statement use in the example.

Short-term stock prices are influenced by the mood-swings of traders and speculators, but in the long term the stock market will price enterprises in line with their intrinsic values. If you want succeed in investing, you need to do your homework and analyse companies to identify the ones that will deliver over the long term.

Company Earnings

Spread betting traders start their fundamental research by checking how much profit a company is netting for its owners. An investor who buys stock from a company becomes a part-owner, so naturally it makes sense to check how much money the company is actually earning.

Here is a summary of the types of profit:

- Sales Revenue = Price (of product) X Quantity Sold

- Gross profit = sales revenue – cost of sales and other direct costs

- Operating profit (EBIT, earnings before interest and taxes) = Gross profit – overheads and other indirect costs

- Pretax Profit (EBT, earnings before taxes) = operating profit – one off items and redundancy payments, staff restructuring – interest payable

- Net profit = Pre-tax profit – tax

- Retained earnings = Profit after tax – Dividends

Always check the operating profit (EBIT), as well as the pre-tax profit. This can normally be found in the company’s cash flow statement. A healthy rise in operating profit is a great sign. However a decreasing or stagnant operating profit is a bad sign.

Do not get this figure confused with operating cash in-flow, or net cash from operating or trading activities. That figure includes amortization of intangible assets, interest and everything else, which inflates the figure, and to be honest it can be ignored year to year. I don’t care if that figure is lower or not because it can be lower one year and they can still have higher revenues and profits regardless. Focus on pre-tax profit and operating profit.

Markets are efficient” – when buying or selling a security it’s important to remember that no matter what upside you’ve envisaged in a trade, the current tradable price is the fair value of the purchased security, any price action after that is based around the events that you may or may not have anticipated.

Price/Earnings (P/E Ratio)

The Price/Earnings examines the share costs in relation to the earnings per share. It is computed by dividing stock price by the earnings per share (EPS) after tax has been deducted and is expressed as a ratio. The fundamental ratio that divulges this information is referred to as the price-to-earnings ratio, or P/E ratio and this is probably the best known indicator (as well as being the most frequently used) since it allows investors to compare different companies very easily. In a nutshell the P/E Ratio displays ‘at a glance’ the number of years it will take the enterprise to generate profits equal to its market cap.

When an investor buys stocks that have a high P/E value, they are expecting average earnings to expand over the course of the investment – it’s up to them to decide whether those earnings will materialise or not. When an investor buys a rental property, they have the choice to overpay, if they are convinced the rent they can charge will increase substantially over time.

A share trading at $5.00 and earning 25c a share is trading at 20 times earnings. A PE can also be negative which would mean that the company is loss-making in which case the next step would be to find out why (the company could be cyclical or a start-up like a technology stock with initial heavy investment or the loss would be due to write-downs). All said, the P/E Ratio is one of the most popular valuation measures (current and futures earnings) and although the Price/Earnings measure is a useful measure it should not be used in isolation as other metrics and financial performance data are needed to put the ratio in to proper context.

Company PE’s are often compared to:

- The multiple on the broader market: or a specific index like the average P/E of the S&P 500 or some other benchmark index to get an idea of how richly a stock is valued in relation to the broader market. For instance the FTSE All-Share trades on a Price/Earnings of 10.4 for 2011 so one can say that any company trading on a Price/Earnings ratio less than this would be considered cheap while a company operating at a premium must have something to deserve this rating in respect of its earnings growth, cashflow, management quality, track record and overall strength of its business model.

- The multiples of peer companies: The P/E ratio is obviously useful when compared with the P/Es of other similar companies to see how the competitors stack up. A high P/E is an indication of high confidence in a company’s future potential.

- The historical multiple of the share itself: this is especially relevant for cyclical companies that may lose money at the trough of the cycle but make loads at the peak. In this instance, using an average EPS figure across a cycle might highlight suitable candidates that are oversold at the trough when the company is operating at a loss (and a normal PE would not really work) or overbought at the peak.

- Relative to growth. Dividing a Price/Earnings by the forecast EPS growth figure returns the Price to Earnings Growth ratio, or PEG [PEG = (Forward P/E Ratio) / (5-Year EPS Growth Rate)]. The PEG ratio helps to highlight whether a stock’s P/E has gotten too high by providing you with information of how much investors are paying for a company’s growth. For example, if a company has a forward P/E of 20 with annual earnings estimated to grow 10% per year on average, its PEG ratio is 2.0. PEG explain how an enterprise can trade on a Price/Earnings ratio double that of another company if it offers twice as much EPS growth. Similarly here, the higher the PEG ratio, the more relatively expensive a stock is. A ratio below 1 is generally considered positive and that the company is trading at a low valuation relative to its growth prospects, while one over 1.5 times is a bit over the top. A company can have a high double-digit PE ratio but still be good value if it is set to grow earnings per share (EPS) by even higher double digits. Of course A PEG ratio could also be low because earnings growth is about to slow or reach a cyclical peak which wouldn’t be good. A PEG less than zero doesn’t mean anything and should be disregarded. Note that the PEG ratio shouldn’t be considered for companies with high levels of debt as the measure ignores debt from the equation.

Price/Earnings Ratio: Share Price/Earnings per Share (EPS)

In practice you can also compute the P/E by dividing the company’s market capitalisation by net income. This is because the P/E ratio represents the number of years the company will take to earn its market capitalisation, assuming annual profits remain steady. P/Es can also be negative meaning the company is operating at a loss.

Note: A PEG ratio divides the PE by forecast earnings growth and this could be low because the company’s earnings progress is about to stall or reach a cyclical phase. This might imply that the company is a bad investment as a falling EPS could also mean a falling stock price.

Earnings per Share (EPS Ratio)

The fundamental data that alert investors as to to how much money the company earned for each share is referred to as the earnings-per-share, or EPS and this figure will be clearly displayed in the company accounts. Brokers also commonly forecast this figure for future years. To calculate the EPS, investors take the company’s overall earnings and divide them by the number of shares the company has issued. If a company earns £1 billion and has 1 billion shares issued, the company’s EPS is £1.

Earnings per Share: Annual Net Income/Number of Shares in Issue

In a nutshell the Price/Earnings ratio provides traders with an idea of whether a stock share is relatively overpriced or underpriced to its counterparts, which is important for traders who are looking to buy or are looking for bargains. In theory, the lower the Price/Earnings ratio, the cheaper the stock but care still need to be taken. For instance, if a share has an EPS (earnings per share) of £1 and the share is trading for £20 then it has a P/E ratio of 20. By checking historic P/E ratios, traders can quickly assess whether the current P/E ratio of 20 is relatively high or low.

High P/E stocks tend to experience higher growth rates and/or the expectation of a profit turnaround. In contrast, low P/E stocks tend to have slower growth and/or lesser future prospects. Generally speaking the lower the P/E ratio, the cheaper and more attractive the stock although the truth may be more complex than this. If a stock is trading at a discount there is usually a reason for this; for instance a low value may mean that the market doesn’t trust the company’s earnings forecasts which could simply be too optimistic or the company may have a weak balance sheet or inherently unpredictable earnings stream…etc

A few words on earnings multiples. Caution is suggested where the market cap of a company is more than 15 times pre-tax profits. You don’t always need to follow this rule but nonetheless I think it’s a good rule of thumb especially in the current climate. Of course you need to compare like with like. Very often there is good reason why one company is on a higher or lower multiple as currently with BP. You also have to be careful with companies operating on Low P/E ratios as there are usually reasons for that.

Also back in the nineteen eighties earnings multiples were much lower than they are today – the effect of a long term secular bear market over several years. The prices range for several years even as earnings increase, but the long term effect is that the multiples decrease. So a multiple of 15 now could fall back to eighties level of 7-8 over several years. I clearly remember House Builders (even the bigger ones) around 2000 were trading on multiples of 4-5 x earnings. If you check out BVS (one of the biggest back then) for 2002 – EPS 62p, S/P average 400p = PER 6.5 If you put today’s BVS on a multiple of 6.5 their share price would be 45p instead of 345p. That is because other factors such as cash and assets (land banks) have to be taken into account.

Price to Sales

Another gem from Security Analysis that puts a completely different viewpoint on using Price to Sales, something I’ve never found useful in the past:

Price to Sales might not be an adequate absolute valuation metric (companies in different industries will have vastly different margins and expenditures, and ultimately, it’s only profits not sales we invest in businesses for).

But the inverse measure of this, Ratio of Sales to Market Cap, offers an interesting operational “gearing” type of statistic. At the margin, if you get a ratio like $2 of sales per $1 of stock, then every extra dollar increase or decrease in sales attributes that much more vividly to the owner.

It can be a sign of a stock particularly exposed to changes in the underlying business – whether in a recovery or a downturn.

It’s a “speculative advantage”, and can apply equally to high or low quality stocks, wherever turnover might change materially over time.

Cash/Cash Equivalents versus Free Cash Flow

Cash and cash equivalents comes from the current assets section of the balance sheet. Effectively this consists of money in the bank, or which could be in the bank quickly if necessary. To be of any use you have to net this off against any debt, and also look at current debtors and current creditors to see whether this is a meaningful figure. If it is still “positive” then this can be taken as a part value of the company. i.e part of the market capitalisation of the company. Useful when valuing companies and looking for takeover targets etc.

Free cash flow comes from the profit and loss account and is effectively the pretax profit of the company adjusted for non cash items like amortisation and depreciation, then remove any new money spent in those areas which will be amortised in the following years. This is the figure you need to compare to earnings per share. For a “mature” company then cash flow per share (CFPS) just above earnings per share (EPS) is a reasonable position to look for, ideally over a few years to balance out any new expenditure. With small companies you need to do a bit more digging to see where the cash goes to make sure they will not need more financing (debt or an equity placement) in order to grow (or even survive).

There is no such thing as a specific good or bad number to look for, it is all sector/industry dependent.

Operating Efficiency

Once traders and investors have inspected the amount of profit that a company earns, they also tend to look at how efficiently the company is run. Shares in efficient enterprises tend to outperform shares in inefficient companies for obvious reasons; since efficiency usually leads to bigger profits and greater earnings flow into owners’ pockets.

For instance margins tell us the proportion of an enterprise’s revenue which is retained as profit. So if a firm generated annual profit of £120 million on revenues of £1 billion it would have a margin of 12%. Margin is sometimes referred to as ‘return on sales’.

One thing to consider in this context is shareholder equity. Shareholder equity is basically company cash, assets and earnings which the company uses for future investment. Investors tend to be interested in equity because if an enterprise cannot efficiently use these assets, they would be better off invested elsewhere.

To monitor the efficiency of asset utilisation, analysts use a comparison figure referred to as the price-to-book ratio. To work out a company’s price-to-book ratio, you need to know the book value of the company, which equates to the shareholders’ equity divided by the number of shares the company has issued. Book value (also known as net asset value – NAV) is the amount of money that would result if a company’s tangible assets were to be sold at their balance sheet value and all liabilities were settled. If a company has £4 billion in assets and issued a total of 1 billion shares, the company book value is £4 per share. Next divide the current share price by the book value to get the price-to-book ratio. If the share trades at £20 its price-to-book ratio is therefore 5. In a similar way to the P/E ratios, price-to-book ratios can help compare whether present share prices are cheap or not. NAV is particularly useful for looking for potential takeover plays since if the market valuation of a company is lower than its book value this in theory would mean that an acquirer could buy out the company and proceed to sell the company’s assets for a profit. However, there are various reasons why a company might be trading at a discount to NAV (say, illiquid assets or uncertainty regarding the company’s future) and these need to be considered.

Enterprise Value

This is computed by adding a company’s forcasted debt and subtracting its forecast cash position from its market capitalisation. This would tell potential investors how much it would cost to acquire the business. Acquirers often reference EV multiple when they evaluate how much to pay for an enterprise. EV multiples are sometimes used by potential acquirers to work out how much to pay for an enterprise.

“I will use market measures” – making use of P/E ratios, Earnings Per Share expectations or generic broker consensus can be invaluable to any investors or traders strategy. Banks pay hundreds of thousands of pounds to analysts to evaluate asset classes. The time they have to commit to analysing a security in comparison to yours, is likely to be far greater, so therefore it is important to consider the opinions of others.

Do Successful Traders focus on Technical Analysis or Fundamentals?

Question

Question: So what is the difference between “operating profit” and “profit before tax”? I’ve tended to ignore the operating cash flow section of results in general because as long as the profit before tax and revenue was increasing, I don’t care how much they’re bringing in from year to year.

However, after seeing the devastating effect that a statement today by XCH had to its share price after they said their “underlying operating profit will be below the lower end of the current range of analysts’ estimates for 2011”, I’m confused as to how that differs to pre-tax profit? The two figures don’t appear to be the same in statements, and normally, analyst’s estimates usually concern themselves more with pre-tax profit. Please explain.

Answer: I can say that the prime difference between operating profit and pre-tax profit is usually the write down of “goodwill” which arises when you overpay for a company that you take over. Operating profit is a cleaner estimate of what is going to repeat in future years ignoring the baggage of the past managements’ impatience and greed. (Organic growth rules OK!).