Global mining giants focus on shareholder friendly initiatives as commodity prices remain subdued

Aug 18, 2014 at 7:19 am in General Trading by contrarianuk

Shares in the larger mining stocks have been pretty volatile of late driven by concerns about China and commodity prices. However, there are signs that the era of big spending with expensive trophy projects is being curtailed with speculation that two of the largest global miners, BHP Billiton and Glencore could announce share buy backs this week. A promise to return capital through either share buybacks or special dividends would signal to investors that global diversified mining houses expect a big increase in their free cash flow and are planning only relatively modest capital spending on new projects.

This contrasts with the situation a few years ago when growth in huge Chinese demand made production growth the priority even if the economics and shareholder returns seemed dubious. Glencore said recently that ‘Any surplus capital, subject to maintaining an efficient balance sheet will be returned to shareholders, within an appropriate timeframe and structure’, leaving the door open to a potential cash return.

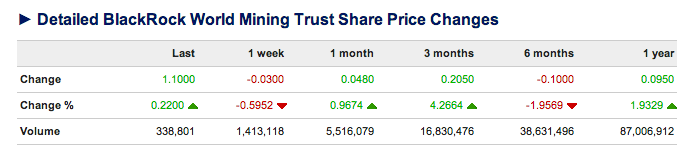

The performance of the Blackrock World Mining trust over the last 3 months illustrates the point that investors are more hopeful for the sector after a poor 2013.

But despite the optimism about the financial management within companies like BHP Billiton and Rio Tinto, worries remain about commodity prices after Chinese demand has slowed in recent months. In particular iron ore prices have been weak. Iron ore prices closed last week at $93.40 a tonne, that’s a 31% drop from the early January price of $135 a tonne, which was also the average for 2013. Higher cost producers have found the rebasing painful, whilst low cost miners particularly those based in Western Australia have increased production to offset low prices.

Last week, mining giant BHP Billiton confirmed that it is likely to proceed with a demerger of its assets, the majority of which were acquired from Billiton back in 2001 to simplify its global portfolio. The company had considered several options, but confirmed that ‘The board has continued to study various structural alternatives including at its meeting this week. A demerger of a selection of assets is our preferred option.’ The demerged assets are likely to include aluminium, manganese and the nickel division. BHP’s South African thermal coal assets could also be included.

BHP board is selling the deal on the basis that after a demerger BHP would focus on its higher margin coal, copper, petroleum and iron ore businesses, with higher returns for shareholders. “We believe that a portfolio focused on our major iron ore, copper, coal and petroleum assets would retain the benefits of diversification, generate stronger growth in cash flow and a superior return on investment. By increasing our focus on these four pillars, with potash as a potential fifth, we will be able to more quickly improve the productivity and performance of our largest businesses.”

A decision on a demerger, which would be likely to see BHP shareholders handed shares in a new listed vehicle, could be made as soon as next week when the board meets to agree the final financial results for the last 12 months . BHP’s earnings are expected to be up for the first time since 2011 driven by growth in production, offsetting weakness in commodity prices.

During the last two years the company has embarked on a series of divestments totaling around $6.5 billion in value and several projects including Nickel West business in Western Australia remain earmarked for sale remain unsold.

Some analysts have questioned the deal, particularly the long term implications of having a company so dependent on iron ore and steel making with the price of the underlying commodities with the remaining divisions (iron ore, copper, coal and oil) under pressure. Are the proposed assets being divested really being materially under managed and therefore undervalued, within the existing structure?

So after a wave of consolidations in recent years, it looks like the era of demergers and asset sales is firmly on the agenda for now. China and South East Asian demand remains key for now with many commentators not expecting a dramatic bounce in commodity prices for the foreseeable future. Any signal to return cash to shareholders will be keenly watched by investors and this week’s BHP Billiton results will be the first acid test of board aspirations.

Contrarian Investor UK

IMPORTANT: The posts I make are in no way meant as investment suggestions or recommendations to any visitors to the site. They are simply my views, personal reflections and analysis on the markets. Anyone who wishes to spread bet or buy stocks should rely on their own due diligence and common sense before placing any spread trade.